The Lines That Never Faded: How Redlining Stole Generations of Black Wealth

When we talk about racism in America, it’s easy to picture the visible signs — the “Whites Only” placards, the segregated buses, the fire hoses. But the most destructive form of racism was drawn in quiet ink, on city maps in the 1930s, when the federal government decided who deserved the American Dream — and who didn’t.

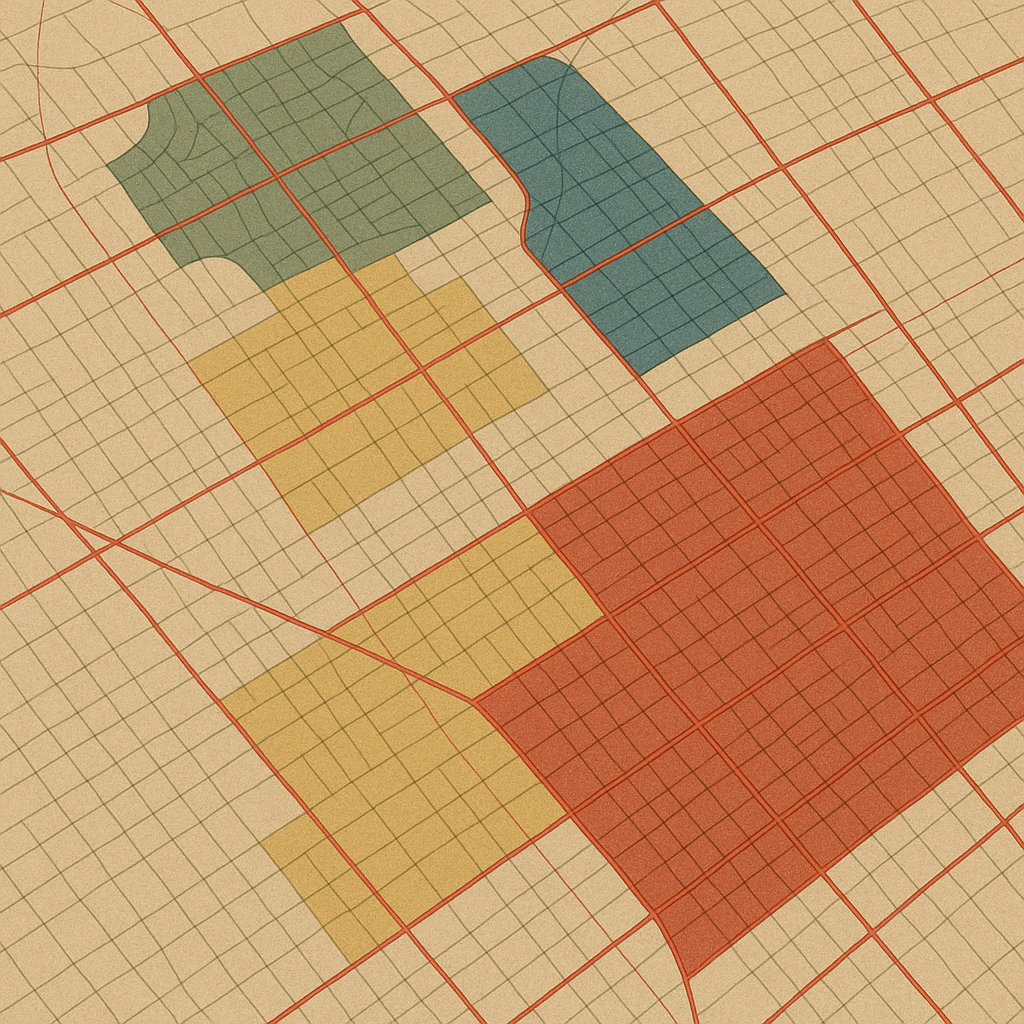

During the Great Depression, the federal government created the Home Owners’ Loan Corporation (HOLC) to stabilize collapsing housing markets. Between 1935 and 1940, HOLC agents graded more than 200 U.S. cities, marking neighborhoods as green (“Best”), blue (“Still Desirable”), yellow (“Declining”), or red (“Hazardous”). A 1937 HOLC report described one redlined area of Philadelphia this way: “Colored infiltration is a definitely adverse influence on neighborhood desirability.” The presence of even a single Black family could lower a neighborhood’s rating. It wasn’t crime or poverty being mapped — it was race.

These color-coded maps soon guided Federal Housing Administration (FHA) policies, which refused to insure mortgages in redlined areas. The FHA’s 1938 Underwriting Manual openly stated, “If a neighborhood is to retain stability, it is necessary that properties shall continue to be occupied by the same social and racial classes.” This wasn’t passive bias; it was official U.S. government policy, institutionalizing segregation and economic exclusion.

From 1934 to 1962, the federal government backed over $120 billion in new housing loans. Less than 2% went to nonwhite families. White Americans received low-interest, government-backed mortgages that allowed them to buy homes in booming suburbs — homes that would become the foundation of generational wealth. Meanwhile, Black families were forced to rent in segregated urban neighborhoods, paying higher rates for worse housing. Sociologist Keeanga-Yamahtta Taylor notes, “The federal government did not simply fail to help Black families; it actively built white wealth while excluding them.”

By the 1950s, entire cities were shaped by these decisions. In Detroit, Chicago, Philadelphia, and Baltimore, the red lines hardened into invisible walls. Even after the Fair Housing Act of 1968 made overt housing discrimination illegal, the damage was done. The neighborhoods starved of credit and investment remained blighted, while white suburbs flourished.

The damage from redlining wasn’t temporary — it was generational. A 2018 Federal Reserve study found that the average white family today holds eight times more wealth than the average Black family. In 2020, the median net worth of white households was $250,400, compared to $24,100 for Black households — a gap largely rooted in housing. A 2022 National Community Reinvestment Coalition study found that 74% of neighborhoods once graded “hazardous” by the HOLC are still low-to-moderate income, and 64% remain majority nonwhite.

Redlining didn’t just rob Black families of homes — it denied them security, health, and opportunity. The effects are visible today in schools, healthcare, and even air quality. Formerly redlined neighborhoods have higher rates of asthma, lower life expectancy, and less access to green space. “Where you live determines how long you live,” says Dr. David R. Williams, a Harvard public health researcher.

What began as lines on a map became the architecture of inequality. Redlining built the suburbs for white families and the ghettos for Black ones. It shaped everything from policing to education funding, from wealth accumulation to neighborhood safety. The Fair Housing Act may have erased the maps, but not the reality they created.

In the end, redlining wasn’t just a housing policy. It was an economic caste system — one that drew its power from paper and ink, and whose consequences still define the geography of American life. The lines may have faded from the maps, but they remain carved into the foundation of the nation itself.